An OIL PRICE drop and US leverage

How the decline in oil price could create an opportunity for greater US leverage and influence around the world

25 March 1983

MEMORANDUM FOR:

- Secretary of State

- Secretary of Defense

- Secretary of the Treasury

- Secretary of Commerce

- Assistant to the President for National Security Affairs

I asked for the attached memorandum on how the decline in oil price could create an opportunity for greater US leverage and influence around the world.

Overview

A sharp drop in o.il pzzices would create an environment that, in general, would work to U S favor. How this translates into specific lines of influence or leveraqe is d.iF.Ficu.Zt to measure. Manu of these opportunities would arise because of the adverse impact oF lower oil prices on the USSR.

- Soviet hard currencq earnings would drop sharp1u—hu as much as $7 billion with $20 oil—forcing Moscow to cut mifitaru and economic aid to client and would—be client states.

From a regional perspective, the pzimaru opportunities created bu lower oil prices are in su_b—.S’aharan Africa.

- In West Africa, Moscow mau he even less able to maintain its position in Guinea and would have trouble exploiting the situation in flhana.

- In southern Africa, the Soviets would have to toughen terms o.n militaru assistance, and the Cubans cannot take up the slack.

- Moscow is alreadu doing this in Tanzania and Zam hia. with ‘T’anzania’s economu in a tailspin, the United States mau have a.n onpor.-tunitu to sour the Tanzanians on the socialist model.

- Angola would suffer a ma_7’or loss in revenues From oil, which is alreadu providing an opening For Western assistance.

- There mag be a similar opening in Mozambique.

- In the Horn, we see no prospect For oil-related changes aFFect.incr the status of Ethiopia or Somaliaias long as the USSR continues to give some aid to the form er.

In Latin A merica, we see only lim.ited opportunities to enhance Us influence.

- The United States is alreadu helping Finance the Mexican and Prazilian economies. We doubt that even another SS billion would huu much more leverage than now exists.

- Venezuela mau offer more opportunities because 0F its connections in Central A merica and the Caribbean. As Venezuelan Funds dry up, the United States could use Caracas to Funnel aid to El .Salvador and others.

- In Suriname, the Cuban hold is Far From Firm. Castro renortedlu does not want to com mit much moneu because oF his own economic nzrohle ms and his concern that Bouterse’s revolution mau be reversed.

South Opportunities and Southeast for Asia. leveracre uniauelu .related to an oil price decline a ppear Few in South and Southeast Asia.

- Indonesia will require large-scale assistance—-either directlu or throucrh banks and the IM F. Providina the moneu mau .not enhance our .ini”l.uence_. but withholding it or .im posing tight cond.itiona.litu might create insta hilitu.

- In Pakistan, the United States mau he called upon to make up shorti”‘alls in Saudi aid. and other oil—related revenue sources.

- As for India, we do not believe an oil price dec.line would create anu good opportunities to exploit.

A steep oil price drop would Jikelu present more pitiialls than opportunities in the East.

- It would destabilize the alreadu tenuous alliances among the countries in the region.

- The Saudis would feel more vulnerable to Iranian and Lihuan attem pts to foment unrest or worse.

- A major risk is that the Saudis will cut air? to i”‘riend_l.u governments a.nd ~ groups faster and bu larger incre m ents than the Li huans cut theirs. Qadhafi would be able to maintain his terrorist and subversive activities at current levels.

- The chief opportunities for the United States would stem From whatever erosion there is in Moscow’s ahilitu to maneuver in the reaion.

In the case of our industrial countru allies, we cannot identifu anu specific leverage that would result from a large drop in o.il prices, but we can see two potential prohle ms.There could be a ma7’or shift in West European attitudes to ward development of North Sea gas; .it would he more d.iFFicult to iustitu on stnictlu financial grounds if oil prices dropped. .Tn this case, Roviet cas— particularly in the l990s—-would become more attractive.

- In an environment of economic recoveru and reduced oi.l prices, the “est Europeans might want to resume large loans to the ll.*?S‘l? and Eastern Europe, in part because much of the reduction in Foviet oil revenues would translate into reduced purchases in Western Europe.

In league with our allies, there is a potential For usino the oil exportino Countries’ need for financial assistance as a lever to obtain their co m mitm ent For mini m u m levels of oil production. Otherwise, the IMF and the industnfal countries would in e*‘Fect he subsidizing OPEC. To sell the notion of oil production requirements heinc associated with international financial support, it could he couched in terms oi’ having the recipients do everything theu can to help themselves.

An OIL PRICE drop and US leverage

A sharp drop in oil prices would spark far-reaching changes in the international economic and political order. What this would mean in terms of US influence is difficult to assess, but it does mean that the nature of US strategic concerns would shift, perhaps substantially in some parts of the world. For one thing, those countries dependent on oil sales for their well-being would see their economic and political power sharply eroded; some could experience internal unrest. In turn, nations that rely heavily on financial flows from the oil producing states—whether in the form of aid, export earnings, or worker remittances—would likewise see their economic situation deteriorate. Countries that are net oil importers will benefit, but for many their economic and political problems are so deep-seated that even a substantial cut in oil import costs would do little to brighten the outlook.

In a more general sense, lower oil prices—by lowering inflation, reducing interest rates, and spurring economic growth—will strengthen the US economy and therefore the US Government’s ability to pursue foreign policy initiatives. The overall stress on the international financial system should ease, lightening the burden the United States carries as the primary lender of last resort. While financial strain will increase in major oil producing LDCs, this need not, if carefully managed, negate the benefits of lower oil prices for the oil importers. In the same vein, lower oil prices in time should lead to an expansion in world trade, which will contribute to more rapid economic growth. US business would then be in a better position to seek out trade and investment opportunities, particularly in Third World economies that have been constrained by high oil import bills and debt.

A major benefit accruing to the United States from a sharp drop in oil prices would be the prospect of greatly reduced hard currency earnings for the Soviet Union. As it is, the Soviets earn over half of their total hard currency from sales of oil and gas; they earn on average another 5–10 percent from gold, the price of which has plummeted recently. As these earnings shrink, the USSR will have to choose more carefully those countries or groups it wishes to support, and Moscow would likely offer less generous terms for aid and military sales. In addition, Soviet surrogates like Cuba could face reduced levels of support which could act as a constraint on their activities.

At a minimum, however, the relative change in US/Soviet economic strength could have an important psychological impact on developing nations. For one thing, a forced Soviet retrenchment would lessen the allure of the Soviet model. For another, a relative rise in US economic power would likely assure Washington greater access as a variety of countries look to the United States for assistance in getting back on the growth track.

Africa

We believe lower oil prices will create problems for the USSR and that, as a result, new opportunities may open up for the United States in Africa. While we do not anticipate that the Soviets will pull up stakes anywhere, a reduced Soviet presence could make some governments more amenable to US overtures or lead to requests for US military or economic assistance. At the same time, however, any oil-related instability could provide Moscow and its surrogates with opportunities for meddling that might not otherwise occur.

- The export of weapons is the most important instrument of Soviet policy in the Third World, and the USSR sets lower interest rates and longer repayment periods for arms sales than Western suppliers. Now, however, we have reports that in two cases this year—Tanzania and Zambia—the Soviets have suspended or threatened to suspend arms deliveries until the buyers make payments. The declining price of oil may be contributing to Moscow’s tougher stance.

- Moscow’s traditional unwillingness to provide large amounts of economic aid to the Third World has been a handicap in trying to win influence, particularly in impoverished African states. Offsetting this handicap through military aid may now be more difficult. Should opportunities for Western economic assistance or political support arise, France could be urged to strengthen its role. Paris has already stepped in to check developments that threatened to advance Soviet interests in Zaire, Chad, and portions of West Africa.

- We believe some of the greatest prospects for Soviet losses in Africa over the next several years will be in Namibia, Angola, and Mozambique. The Soviets have already tried to impede Western mediation efforts on Namibia, in part through offers of military aid intended to induce key African leaders to oppose the negotiations. These aid offers may have to be trimmed. In Angola, which has been hurt by the drop in oil prices, the Soviets have refused to reschedule debt. In Mozambique, the South African-backed insurgency has made the Machel government increasingly dependent on Soviet and Cuban support. If this trend continues—and particularly if Cuban combat forces were sent to Mozambique—the Soviets would probably find Machel more responsive to their interests, such as gaining naval access rights. If Moscow were to reduce aid and oil deliveries to Cuba, however, Havana might become more cautious in making commitments in Angola as well as Mozambique. Moscow would then see its influence being undermined in both countries.

- In the Horn of Africa, we believe that Ethiopia and its Soviet, Libyan, and Cuban backers will still attempt to undermine support for US military access agreements in the area and try to weaken or overturn the governments of Somalia and Sudan. These efforts may be hampered, however, if the Soviets are forced to reduce their commitment. Ethiopia has had disagreements with the USSR over the extent of Soviet financial concessions and oil guarantees, but we believe Mengistu will maintain his close alliance with Moscow. The Soviet connection bolsters Mengistu’s personal power and prestige, and he probably calculates that no combination of Western powers would be willing to replace Moscow as his principal source of military or economic aid without insisting on major changes in Ethiopian domestic policies.

The Siad Barre government in Somalia has little interest in improving relations with the USSR as long as the Soviets continue military aid to Ethiopia.

In addition to the possible opportunities for the United States in Soviet-dominated states, we believe that by far the largest and most direct impact of lower oil prices on US interests in Africa will come in Nigeria. In our judgment, President Shagari will increasingly look to the United States for financial assistance. In most other African countries, lower oil prices will reduce financial strains, but only slightly. They will have to await an upturn in OECD demand for their nonfuel commodities before any marked economic improvement occurs. Partly because of the sad state of their economies, there may be opportunities in several West African countries for the United States to influence the direction their governments take in dealing with the USSR.

- Nigeria, the United States’ third-largest supplier of imported oil, is heading toward its most serious economic crisis since the 1967–70 civil war. We believe President Shagari will be forced to continue or strengthen austerity measures despite the pressures of a general election campaign in mid-1983. In our judgment, sudden additional retrenchment could spark widespread disorder and encourage sentiment for a coup within the military. If dissatisfaction grows during the run-up to elections, Shagari may seek increased sales of Nigerian oil for the US Strategic Petroleum Reserve, a food-for-oil barter agreement, or a substantial emergency loan similar to that arranged with Mexico. The United States, in turn, might encourage the notion among international lenders that Nigeria should maintain a certain level of oil production as a condition for large-scale assistance. If Nigerian leaders are unhappy with the US response, they might become less supportive on the Namibian issue or subject US oil companies to bureaucratic harassment.

- We believe the consolidation of radical control in Ghana could enable Libya, Cuba, and the USSR to gain a sufficient foothold to use the country as a base for subversion of Ghana’s moderate neighbors. The economy continues to deteriorate, and the few policies articulated by the Rawlings regime are unlikely to have much positive impact because they fail to address underlying structural problems. In our view, radicals in Rawlings’s entourage are consolidating their power and will try to align Ghana more closely with Communist states and Libya, with the aim of eventually having Ghana adopt a socialist economic system. What leverage the United States has with Ghana at present derives largely from Washington’s influence with the IMF, which Accra may approach for assistance, and from the modest US aid program, mainly food.

- Guinea’s President Sekou Toure, long one of Africa’s most vociferous radicals and strongest supporters of Moscow, has been expressing growing frustration with the Soviet Union and establishing closer ties with the United States and other Western governments. He has also become a vigorous spokesman for moderate West African states concerned about Libyan interference in regional affairs. Moscow’s failure to provide adequate economic help has contributed to Toure’s strong dissatisfaction with the Soviets, a feeling that could be reinforced if Moscow has to trim its aid. His policies have made a shambles of a once-promising economy and have kept Guinea within the ranks of the world’s poorest countries. To revive the economy, Toure is making some major adjustments in its socialist orientation and is seeking massive infusions of aid and investment, principally from moderate Arab states and the West.

In the near term at least, Toure’s policies probably will remain generally compatible with US interests in Africa. He will support Moroccan King Hassan against Algeria and the Polisario insurgency, promote the influence of moderate states in the OAU, oppose Libyan activities south of the Sahara, and turn aside Soviet requests for a greater presence in Guinea.

- Of the two principal emerging oil producers in Africa—Cameroon and the Ivory Coast—we believe Cameroon stands the best chance of handling a decline in oil prices, largely because it has a strong agricultural sector. Moreover, in our judgment, Cameroon has been more successful than Nigeria or Gabon in handling its oil windfall. As the sole buyer of Cameroon’s oil, the United States may need to do little more than demonstrate concern to ensure a continuation of President Biya’s strong pro-Western stance.

The situation in the Ivory Coast, still a net oil importer, is more tenuous. To the extent that revenues from the emerging petroleum sector are reduced, the risk of a military government replacing aging President Houphouet-Boigny will increase. The country’s oil industry is dominated by US firms, and the government may look to them to intercede with Washington if the country cannot meet payments on its external debt.

Latin America

We doubt that a sharp drop in oil prices would substantially alter US relationships with most Latin American countries. Mexico and Venezuela are the most likely requestors of large—scale US assistance, but in both cases the US Government and/ or US banks already play a dominant role in their financial affairs. Brazil’s payments crisis would be eased slightly, but the problems are so severe that it is already dependent on the United States to arrange official and private financing as well as help secure support from the IMF. In these countries the challenge may be to avoid the appearance of dictating policy and thus diminish US effectiveness.

Argentina, which is self—sufficient in oil, is preoccupied with arranging the transition from military to civilian rule and with carrying out its economic stabilization program. We see little likelihood of lower oil prices doing anything to change this inward focus.

Colombia and Bolivia, as net oil importers, would benefit from a drop in oil prices; any financial leverage the United States might exert to reduce drug shipments would thus be weakened.

- The new Mexican government will have a hard time imposing the austerity needed to bring financial order without disrupting the internal political balance. Recent International Monetary Fund and World Bank projections indicate that without IMF support Mexico would be forced to reduce imports by $5 billion in 1983, in addition to the nearly $10 billion reduction absorbed last year. A large oil price decline would place President de la Madrid in a desperate position. He would probably have to weigh the pros and cons of debt repudiation, which would sharply lower US bank profits and cause some to fail. To maintain US financial backing, de la Madrld will seek to keep US—Mexican relations on an even keel, but we think some grating episodes are inevitable. While he has told US officials that he intends to avoid inflammatory public statements, he has publicly stated he will maintain close ties with Havana and Managua. Given the large role the United States would have to play in Mexico’s economy, Washington might gain some quid pro quos on foreign policy-—particularly on Central American and North—South issues.

- Venezuela would be unable to pursue its domestic economic development program and would have to cut sensitive social programs in the event of a sharp oil price decline. In this election year, however, President Herrera’s austerity program will be at risk from strong party pressures for pork barrel spending. Even if tougher adjustments were undertaken, we think there is a better than even chance that Venezuela will experience a foreign exchange crisis by mid-1983. The worsening problems almost assure a presidential victory in December by the opposition Democratic Action candidate, Jaime Lusinchi, but we doubt the government’s economic strategy will change much. As Venezuelan leaders struggle with economic problems, they will look to the United States for support. Mindful of the role that US firms and lending institutions can play, Venezuela could well be persuaded to mute its frequent posturing as a self—appointed spokesman for the Third World on North—South issues. Domestic constraints will limit Caracas’s involvement in regional affairs; the joint Venezuel.an/ Mexican oil financing facility and regional aid programs will be sharply curtailed.

- Brazil would be the largest LDC gainer from a decline in oil prices, but the drop would have to be substantial to reduce greatly the pressures on the current account. The financial situation is so precarious that we believe the Brazilians will continue having to borrow large amounts in the overnight markets to avert liquidity problems. Beyond this, we think Brasilia will likely soon be forced to seek additional assistance from US banks. In these circumstances, continued US support is essential to avoid Brazil’s declaring a moratorium on debt repayments. If this were to occur, we believe the economy would go into a tailspin. Rising unemployment, real wage declines, and mounting business failures would trigger social unrest. Anything Brazil might do in return for US help might not be worth the consequences of withholding US support.

- The suspension of Dutch aid following the December execution of 15 leading critics of Suriname’s government is raising the prospects for increased Cuban involvement. The Bouterse regime’s frantic Search for funds from several Latin American countries so far has been futile. Bouterse has already warned publicly that he will seek aid from the Soviet Bloc if Western countries do not come through. After a military coup almost succeeded in March 1982, Bouterse turned to Havana for political support. Exploiting Bouterse’s growing isolation and sense of insecurity, Cuba has gained considerable influence. We believe Bouterse’s reliance on the Cubans will continue as long as he believes his domestic position is insecure and does not think Havana is acting against his interests. Various sources have reported that Cuba cannot afford to be very generous and that Havana wants to avoid alienating Western powers as it attempts to renegotiate its debt. Under these circumstance, the Castro regime probably will pursue a low—key expansion of its influence.

- The Central American and Caribbean countries are highly vulnerable to the negative feedback effects of an oil price drop. Growth has already slowed sharply, and increased borrowing to help finance worsening current account deficits pushed the region’s medium— and long-term external debt to $15 billion at the end of 1981. In this environment, access to bank lending is crucial. If the oil price decline impairs bank lending to the region, the impact on their fragile economic and political systems would be serious. The region also stands to lose the aid it has received from Venezuela, Mexico, and Trinidad-Tobago. To the extent that the region faces new stress, the opportunities for Cuban mischief would increase.

South and Southeast Asia

Among the South and Southeast Asian LDCs of strategic interest to the United States, we think lower oil prices pose the greatest threat to Indonesia and Pakistan. An economically weakened Indonesia would provide fertile ground for trouble making by Islamic fundamentalists or other dissident groups. This could force the Soeharto government to focus on domestic politics to the detriment, for example, of ASEAN efforts to achieve a political settlement in Indochina.

Pakistan, although an oil importer, would be hard pressed financially if Saudi aid and remittances from Pakistani citizens working in the Persian Gulf states were substantially reduced. Even so, economic pressures alone are unlikely to affect pursuit of a nuclear weapons capability.

In India, Prime Minister Gandhi apparently is trying to steer a more neutral course between the United States and the USSR than she has in the past; any US move to increase military aid to Pakistan might jeopardize the recent thaw in US–Indian relations.

As for South Korea and the Philippines, we would anticipate no significant changes in their relations with the United States as a consequence of lower oil prices.

- Indonesia would have to cut development spending drastically. The technocrats influencing Indonesian economic and financial planning apparently misread the oil market, and the government has done little to cope with the decline in oil earnings. President Soeharto has cut subsidies for food, fuel, and fertilizers, frozen civil servant and military wages, and reduced other spending, but stiffer austerity measures—including cuts in the country’s previously sacrosanct industrial development programs—will be necessary to avert a financial crisis. We estimate Indonesia will run an $8–11 billion current account deficit this year. In return for U.S. help in arranging financing for the deficit, Jakarta might be persuaded to abandon plans to further restrict the operating environment for foreign oil companies.

- Foreign exchange losses associated with any Saudi retrenchment could result in intense pressures on Pakistan. From General Zia’s perspective, the economic and political balance would be shifted in favor of India, which would see its oil import bill fall sharply. Although India would also experience a reduction in worker remittances from the Gulf and in export revenues, on balance it would fare better than Pakistan. Growing economic and political pressures are unlikely to affect the nuclear program, since Zia views it as a mechanism to maintain regional balance.

Middle East

The Middle East would bear the brunt of an oil price drop. Although the Gulf Arabs’ huge reserve holdings would cushion the impact, lower revenues could constrain their ability to support the Iraqi war effort. The prospect of an Iranian victory could prompt the Saudis to quietly seek closer ties with the United States.

US interests in Iran and Libya would be little served by lower oil prices. With tighter government political and economic control, both have relatively greater flexibility in dealing with a price decline, and both have already reduced imports.

Under certain circumstances, a drop in oil prices could lead Syria to act in ways which coincide with US objectives. Syria receives substantial aid from Iran, the USSR, and the Gulf States. If financial pressures forced a cut in these flows, Assad would probably realign himself with the Saudis and possibly lessen his support for Iran.

- Despite Syria‘s reliance on outside financial support, Assad has not been willing to temper his foreign policy to suit the tastes of his more conservative Arab backers. For now, he can afford to alienate them and run the risk of an aid cutoff, since Syria’s political cooperation is important enough to Iran and to the Soviets that they are willing to extend him adequate economic support. If both Iran and the Gulf states cut their economic support due to their own cash flow problems, Assad would probably view the Gulf states as more dependable and easier marks over the long haul. We expect he would re-ingratiate himself with the Saudis by backing away from his support for Iran, and possibly accede to Saudi pressure to withdraw troops from Lebanon or support a Jordanian–PLO dialogue. US attempts to influence this course of events could well prove self-defeating.

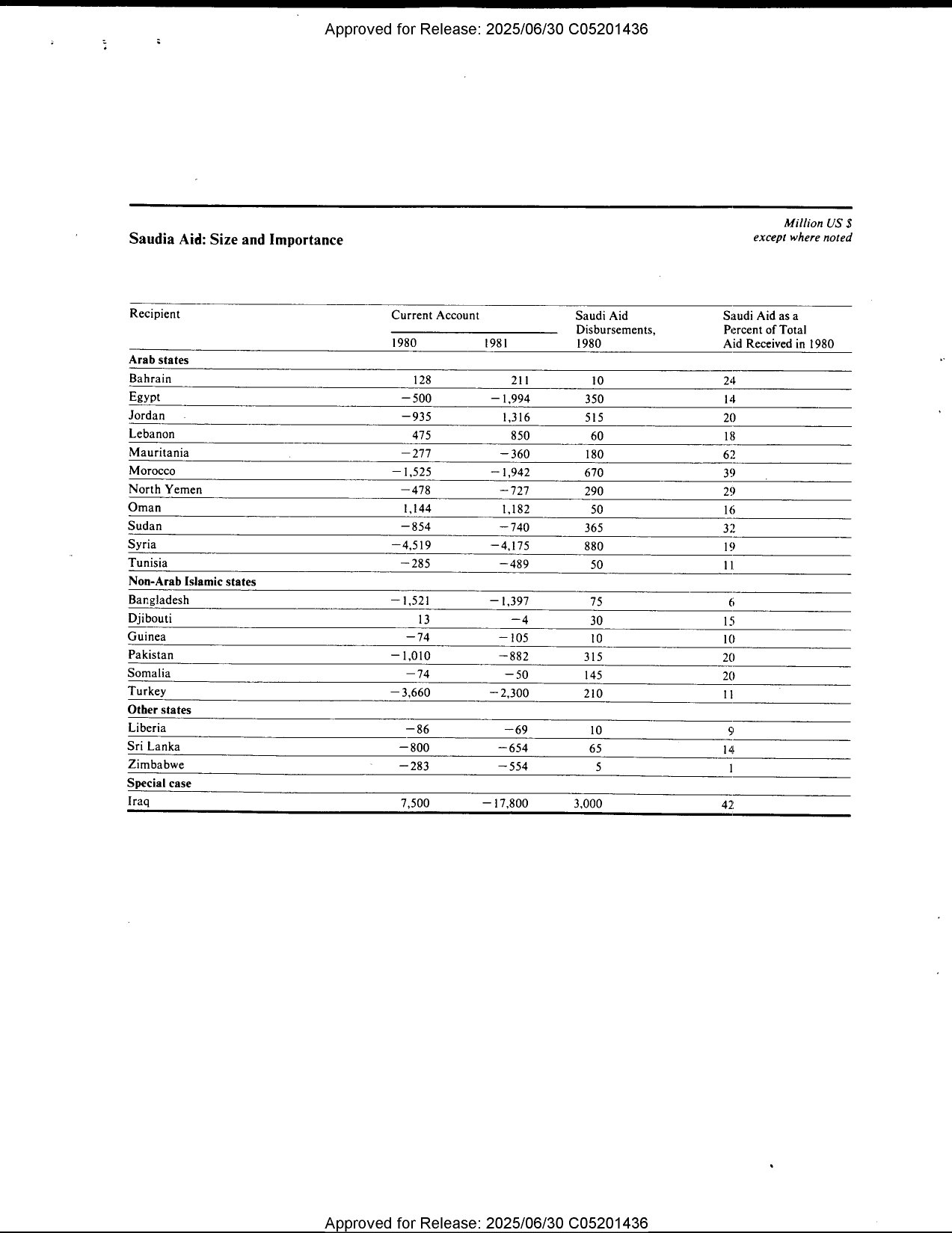

- Saudi Arabia‘s sense of vulnerability to Iranian and Libyan threats would rise if oil prices fell sharply. Riyadh’s limited ability to influence the PLO and the Arab confrontation states through its aid program would also be eroded if aid had to be curtailed. Under these circumstances, the Saudis would be less willing to press Arab radicals like Syria to adopt more moderate positions on important regional issues. The Saudis might also feel compelled to publicly distance themselves from the United States on a broad range of political issues while realizing privately that the United States remains the ultimate guarantor of Saudi security.

- Iran‘s political–economic strategy will be little affected by an oil price drop. Imports remain low because of the limited development objectives of the Khomeini government. Indeed, Iran is able to get along on far less oil revenues than it presently receives—additions to reserves in 1982 totaled some $2 billion. Moreover, the regime could probably cut domestic spending further without any serious impact on internal stability. Iran’s basic hostility toward the United States and its suspicion of Soviet motives will remain regardless of what happens to oil prices.

- Iraq could face more problems from an oil price drop than any other Gulf oil producer. Not only would its own oil revenues fall, but the massive aid from other Gulf Arabs on which Iraq survives would be put at risk. Nonetheless, we believe that an oil price drop would not significantly alter Iraq/US relations. The United States imports virtually no oil from Iraq, and US exports are small. Although Iraq may seek additional CCC credits—these totaled $210 million last year—agricultural credits provide the United States with little leverage.

- Iraq may be a country where the Soviets have decided to target their shrinking aid resources. Reliable sources report that the USSR is willing to negotiate a major arms pact—worth perhaps $1 billion—and to consider concessionary terms. We believe this results in part from the Soviets’ frustrations over their deteriorating relations with Iran. Moscow also wants to ensure an arms market in Baghdad when the war ends and to reverse Iraq’s increased reliance on Western military suppliers. Baghdad apparently hopes to induce Moscow to intervene with Syrian President Assad to reopen the Syrian–Iraqi pipeline. Direct US options are limited, but the West Europeans might be encouraged to counter the Soviet weapons offer.

- Libya would see its export earnings plunge as a result of a sharp decline in oil prices, but we see little likelihood that this would change Qadhafi’s behavior. Libya’s current account was almost in balance last year, and Qadhafi has already implemented a series of austerity measures to slow the foreign exchange drain. Although the retrenchment may be adding to existing disaffection generated by unpopular measures enacted in the past, we believe Qadhafi has the wherewithal to keep the domestic situation firmly in control. Libya’s support for terrorism and military adventures probably has never cost more than $200 million in any year since 1978, and Qadhafi will remain in a position to work with the Soviets if oil-related opportunities for political gain arise in Africa.

- Egyptian oil revenue losses would make US economic and military assistance increasingly important. The Egyptians already are considering reductions in their ambitious economic growth targets, and we believe that Cairo also will have to seriously consider cuts in politically sensitive consumer subsidies and perhaps even military expenditures. Alternatives to US assistance will be less likely as oil prices decline. The Persian Gulf states and the USSR will have other aid recipients that they may deem more important. Thus, even if Egypt overcame the political barriers to renewed aid relationships with these countries, they would not be in a good position to provide much assistance. Furthermore, neither the Arab states nor the USSR have the agricultural commodities—particularly wheat—needed to sustain Egypt’s food distribution programs.

Should Egypt’s foreign payments problems deteriorate to such an extent that Cairo would have to negotiate an IMF program or seek debt relief, Egyptian officials doubtless would look to the United States for relief from official debt payments and for help in dealing with both the IMF and commercial lenders.

- Although Sudan’s current account deficit will benefit from falling oil prices, but Khartoum will still look to the United States for guidance in dealing with the IMF and with official and private creditors. If lower oil prices lead to a reduction in aid from Arab oil-producing states, Khartoum will doubtless seek additional US assistance. Lower oil prices could lead to the postponement of oil production plans that are one of the few bright spots in Sudan’s future. Should this occur, the Sudanese could blame Chevron—a US firm—for the delay.