Suriname’s oil development made possible by IMF, IDB and World Bank public finance (2022)

Action Alert

February 8, 2022

Summary

- December 2021: IMF approved $688 million Extended Fund Facility; IDB Invest

approved $14.5 million for port facility expanding oil services - Upcoming, IDB and World Bank proposing $330 million to $600 million in budget

finance, which can be used for any oil or gas associated expenditures - Early 2022, Total planning $7 billion Final Investment Decision in offshore oil

Block 58, with more oil investment to follow by Exxon (Block 59) - IMF and IDB tax reforms protect big oil profits, increase taxes for others – ultra

low royalty and tax rates for oil investments remain, while tax rates for non-oil sectors

and citizens increase, with the heaviest burden falling on the poorest people - IMF, IDB and World Bank provide critical financial bridge for oil development –

including funding for government costs to manage and serve oil development and for

associated infrastructure. This public finance is vital while there are no oil revenues

coming in and the oil-associated, duty-exempt imports are high. - Since 2019, IDB and World Bank provide technical assistance for oil and gas

development – including geophysical data and gas prefeasibility studies; consultants

for legal, regulatory and permitting support to keep oil development on schedule - Given the IMF, IDB and World Bank are supposed to help Suriname resolve its

debt crisis, pushing over $1 billion in new debt worsens the problem. Upholding

policies for big oil profits is reckless for Suriname’s finances and devastating for

the climate.

The IMF, IDB and World Bank should help Suriname resolve its debt crisis without exacerbating unsustainable public debt and contributing to the climate crisis. Suriname’s economy is highly concentrated on oil and mining (gold and bauxite). Right now, Total, Exxon and other companies are seeking billions of US dollars in new oil investments in offshore Suriname.

The public funding of the International Monetary Fund (IMF), Inter-American Development Bank (IDB) and World Bank must help Suriname become less dependent on oil production, not lead them to be significantly more dependent on it, which is the current plan.

With a largely coastal-dwelling population, Suriname faces significant risks from climate change, which will disproportionately hurt the poor. Ultimately, it is up to the people of Suriname to decide whether or not to develop their oil.

International public funding, i.e., people’s tax dollars, should not be used to support massive profits for oil companies – the perpetrators of climate destruction. Instead, international public finance should be used to offer the people of Suriname an alternative to oil expansion – such as paying Suriname to keep their oil in the ground, including through International Finance Institution (IFI) debt cancellation.

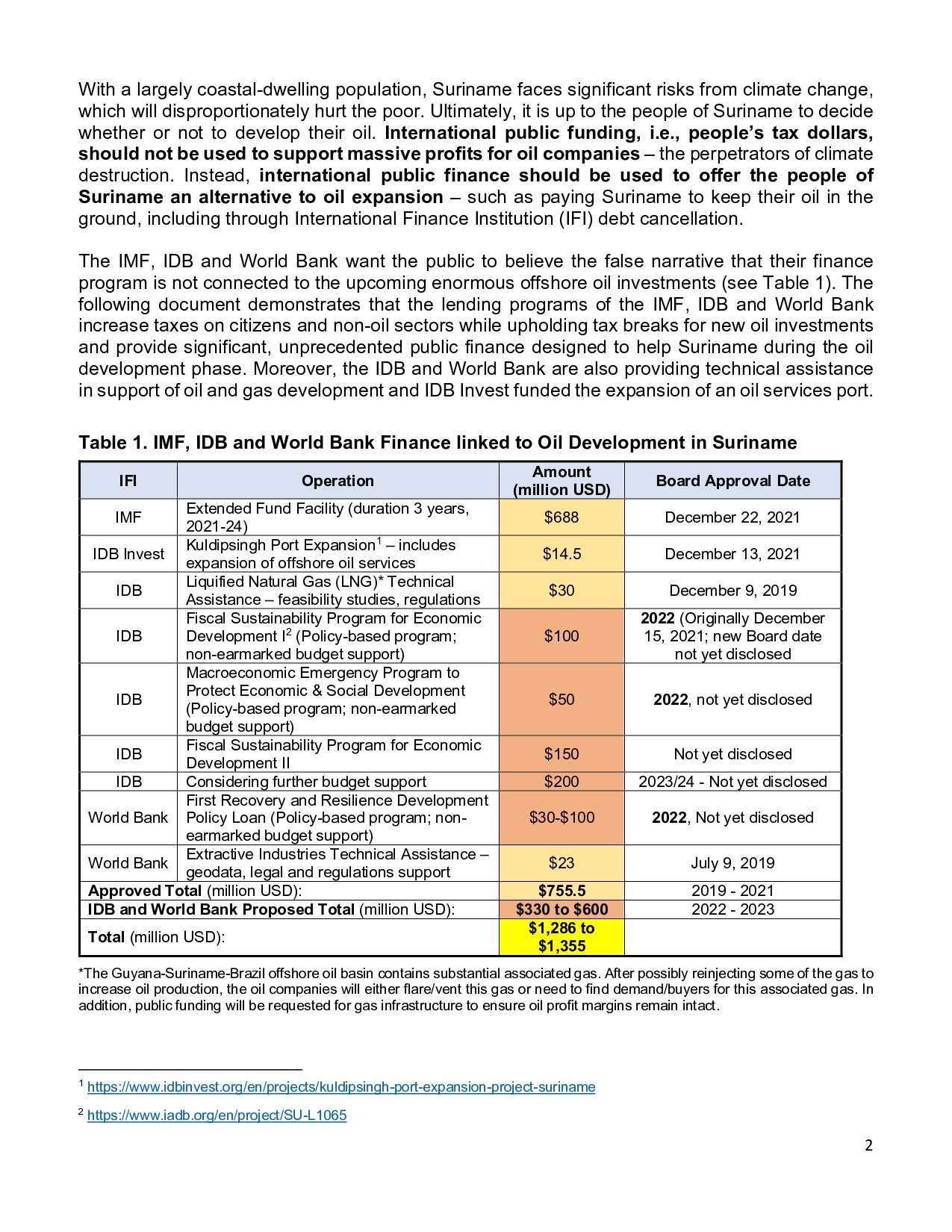

The IMF, IDB and World Bank want the public to believe the false narrative that their finance program is not connected to the upcoming enormous offshore oil investments (see Table 1).

The following document demonstrates that the lending programs of the IMF, IDB and World Bank increase taxes on citizens and non-oil sectors while upholding tax breaks for new oil investments and provide significant, unprecedented public finance designed to help Suriname during the oil development phase.

Moreover, the IDB and World Bank are also providing technical assistance in support of oil and gas development, and IDB Invest funded the expansion of an oil services port.

Table 1. IMF, IDB and World Bank Finance linked to Oil Development in Suriname

| IFI | Operation | Amount (million USD) | Board Approval Date |

|---|---|---|---|

| IMF | Extended Fund Facility (duration 3 years, 2021–24) | 688 | December 22, 2021 |

| IDB Invest | Kuldipsingh Port Expansion (*1) – includes expansion of offshore oil services | 14.5 | December 13, 2021 |

| IDB | Liquified Natural Gas (LNG)* Technical Assistance – feasibility studies, regulations | 30 | December 9, 2019 |

| IDB | Fiscal Sustainability Program for Economic Development I (*2) (Policy-based program; non-earmarked budget support) | 100 | 2022 (Originally December 15, 2021; new Board date not yet disclosed) |

| IDB | Macroeconomic Emergency Program to Protect Economic & Social Development (Policy-based program; non-earmarked budget support) | 50 | 2022, not yet disclosed |

| IDB | Fiscal Sustainability Program for Economic Development II | 150 | Not yet disclosed |

| IDB | Considering further budget support | 200 | 2023/24 – Not yet disclosed |

| World Bank | First Recovery and Resilience Development Policy Loan (Policy-based program; non-earmarked budget support) | 30–100 | 2022, Not yet disclosed |

| World Bank | Extractive Industries Technical Assistance – geodata, legal and regulations support | 23 | July 9, 2019 |

| Approved Total (million USD) | 755.5 | 2019–2021 |

|---|---|---|

| IDB and World Bank Proposed Total (million USD) | 330–600 | 2022–2023 |

| Total (million USD) | 1,286–1,355 | — |

*The Guyana-Suriname-Brazil offshore oil basin contains substantial associated gas. After possibly reinjecting some of the gas to increase oil production, the oil companies will either flare/vent this gas or need to find demand/buyers for this associated gas. In addition, public funding will be requested for gas infrastructure to ensure oil profit margins remain intact.

Guyana-Suriname-Brazil Oil Basin, World’s Biggest New Oil Developments

Big Profits for Oil Companies – Bad Deal for the People of Suriname and for the Climate

Last year, the International Energy Agency (IEA) warned that there can be no more investments in new oil, gas or coal production if we are to limit warming to 1.5 degrees Celsius – the goal of the Paris Climate Agreement. However, big oil companies are ignoring this fact.

Currently, Total, Exxon and partners are getting ready to make final investment decisions in Suriname’s offshore oil blocks worth billions of US dollars. Development of the massive Guyana-Suriname-Brazil offshore oil basin has already begun in the Guyana and Brazil sections. So far in Guyana, over 12 billion barrels of oil have been discovered. The World Bank and IDB have been helping all three countries attract investment into the basin through technical assistance; project finance for associated infrastructure; and budget finance in Guyana and proposed for Suriname.

Exxon, along with partners Hess and China National Offshore Oil Corp (CNOOC), was able to start oil production in Guyana in record time thanks to IDB and World Bank assistance on permitting and geodata along with budget finance to help cover government costs to facilitate the oil development. The IDB and World Bank are taking the same approach in Suriname. Suriname has at least three to four billion barrels of oil reserves in the offshore basin. This amounts to nearly half the new oil and gas discovered around the world last year. (*3) Total and APA (formerly Apache) have made four oil discoveries in Block 58 since the beginning of 2020. In December 2020, ExxonMobil and Petronas announced their first oil discovery in Block 59. At least 15 new wells are set to be drilled in the coming year. Another 30-year Production Sharing Contract was signed with Chevron and Shell in October 2021 for offshore Block 5.

Guyana and Suriname are the hottest prospects for oil companies due to the promise of large quantities of oil at super low development costs. Both countries have signed production sharing contracts with oil companies for very low royalty and tax rates and fast cost recovery (see more details below). Suriname’s contracts are based on a royalty rate of only 6.25 percent. This is less than half the average rate in the developing world, which is roughly 16 percent. (*4) In both countries, the break-even oil development cost is an incredibly low $35-$40/barrel. This means big profits for big oil.

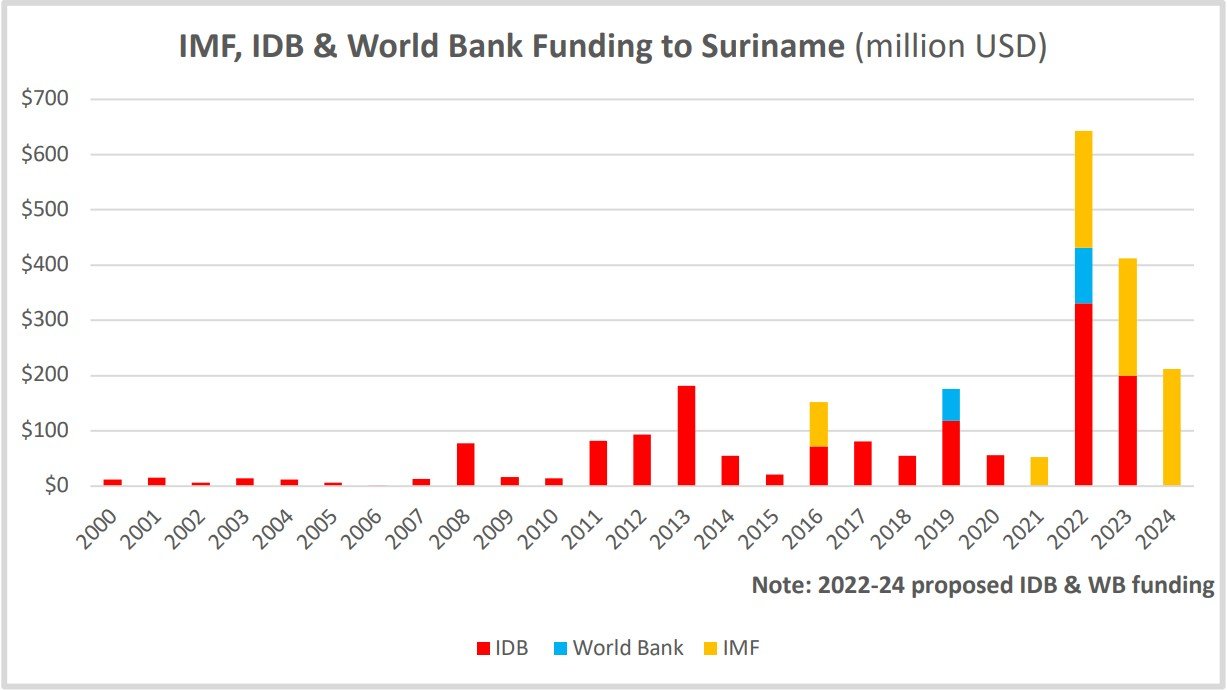

At the same time, Suriname faces great difficulties servicing its public debt. In November 2020, Suriname defaulted on its sovereign debt payments. The IDB is Suriname’s largest creditor. Suriname has turned to the IMF, IDB and World Bank for finance (see Table 1 and Graph 1). In total, the new approved and proposed public debt amounts to $1.3 billion or approximately $2,170 per person in Suriname. (*5)

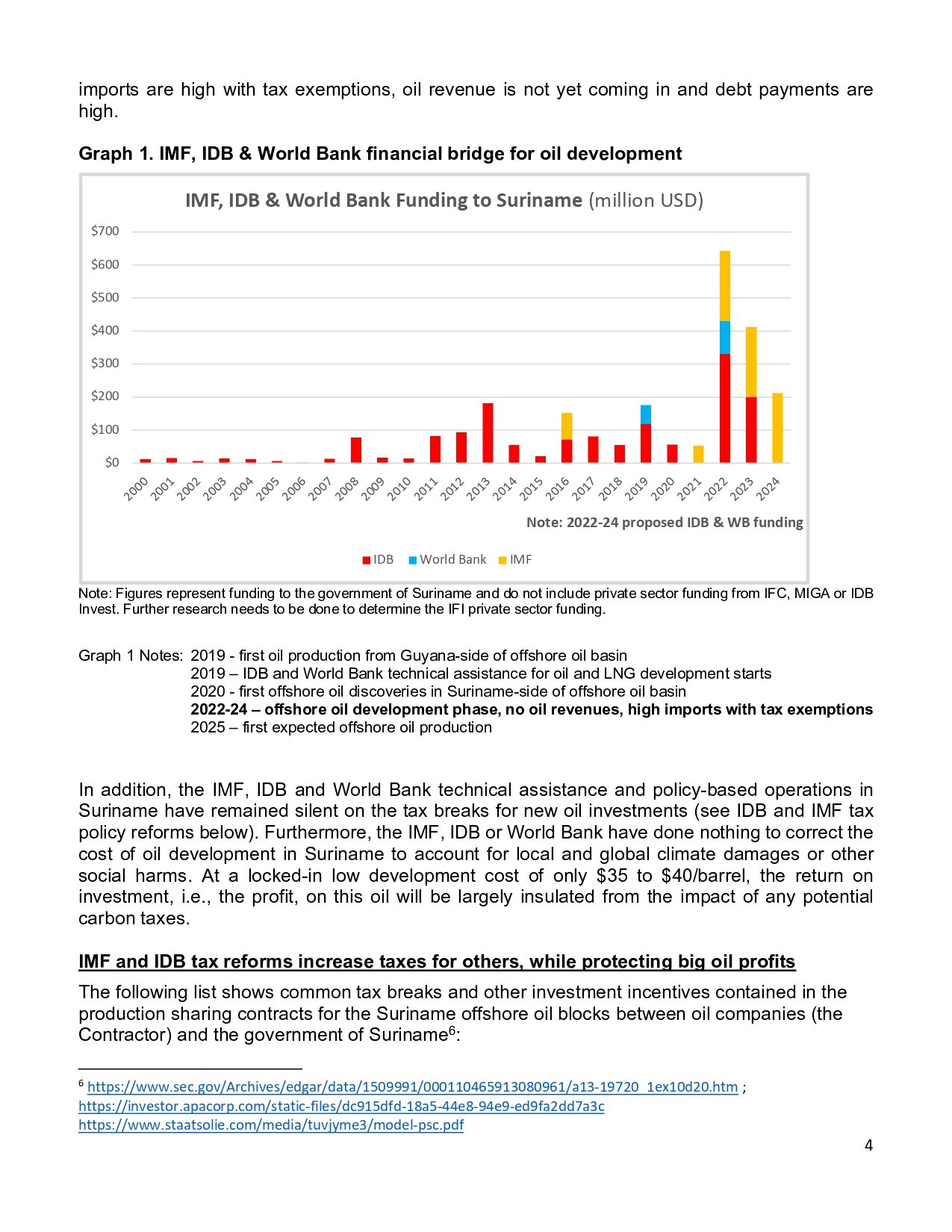

Such a high level of new public debt hardly seems the best way to resolve Suriname’s unsustainable public debt. But it does provide Suriname with access to large sums of funding during the offshore oil development phase (2022-2024), when government costs will be high to facilitate oil development, and government revenues will be low because oil development-related imports are high with tax exemptions, oil revenue is not yet coming in and debt payments are high.

Graph 1. IMF, IDB & World Bank financial bridge for oil development

Graph 1 Notes:

- 2019 – first oil production from Guyana-side of offshore oil basin

- 2019 – IDB and World Bank technical assistance for oil and LNG development starts

- 2020 – first offshore oil discoveries in Suriname-side of offshore oil basin

- 2022-2024 – offshore oil development phase, no oil revenues, high imports with tax exemptions

- 2025 – first expected offshore oil production

In addition, the IMF, IDB and World Bank technical assistance and policy-based operations in Suriname have remained silent on the tax breaks for new oil investments (see IDB and IMF tax policy reforms below). Furthermore, the IMF, IDB or World Bank have done nothing to correct the cost of oil development in Suriname to account for local and global climate damages or other social harms. At a locked-in low development cost of only $35 to $40/barrel, the return on investment, i.e., the profit, on this oil will be largely insulated from the impact of any potential carbon taxes.

IMF and IDB Tax Reforms Increase Taxes for Others, While Protecting Big Oil Profits

The following list shows common tax breaks and other investment incentives contained in the production sharing contracts for the Suriname offshore oil blocks between oil companies (the Contractor) and the government of Suriname (*6):

- Low royalty rate of 6.25 percent, which is less than half the average rate of 16 percent for developing countries (*7);

- Import and export duty exemptions for the Contractor and its Sub-Contractors – all equipment brought in to develop the oil fields and the oil/gas exports, etc.;

- Tax stabilization clause – if there are any changes to tax, royalty, or any other legislation that adversely impacts the Contractor’s economic benefit, the economic terms of the Contract will be modified to maintain the same economic benefit as before the changes;

- Duty-free import of household objects for use by Expatriate Employees of the Contractor, Operator and Sub-Contractors; and

- 80% Cost Oil – 20% Profit Oil – until all costs (exploration, development, operations) are recovered by the Contractor, the amount of crude oil produced is split 80% as Cost Oil to pay back costs and 20% as Profit Oil to be distributed between the Contractor and the government according to an R-factor formula. (*8) The high portion given to Cost Oil significantly cuts into the short- to medium-term profit sharing of the government. It also reduces volatile oil market risks for investors as their initial investment is paid back quickly.

Under the IMF and IDB loan programs, in order to increase government revenues and limit spending, the programs require: increasing electricity tariffs (by reducing consumer subsidies, which has led to social unrest in the past); implementing a new VAT tax (as a source of non-mineral revenue); increasing royalty rates for gold mining (existing contracts will challenge this change); and reducing the public wage bill.

It must be noted that both the introduction of the VAT tax and the reduction of the public wage bill are regressive measures and will fall heaviest upon the poorest women, men and sexual and gender minorities (SGMs) in Suriname. (*9) While according to the IMF, the social safety net is supposed to be strengthened “to soften negative impacts from program adjustments on the most vulnerable” – mainly through a 0.5 percent increase in the cash transfer program – it is impossible to assess the adequacy of this increase and coverage of the poor women, men and SGMs.

Furthermore, the IMF and IDB required measures specifically avoid adversely impacting the profit margin of new oil investments. While the IMF specifically targets the low royalty rates in gold mining contracts, it turns a blind eye to the ultra-low royalty rate for oil contracts. Overall, the IMF and IDB programs increase taxes for citizens and non-oil sectors, while leaving the ultra-low royalty and tax rates in place for oil.

The costs to the public of the IMF, IDB and World Bank programs and the costs to the public of oil development equal a bad deal for the people of Suriname. The people of Suriname will be saddled with very high public debt; increased taxes and electricity tariffs; high oil market risks; high local climate/social/environmental costs; and vastly below market returns from the oil development.

IMF, IDB and World Bank provide vital Financial Bridge for Oil Developments in Suriname

Suriname is a small middle-income country with a population of less than 600,000. In 2016, to help address Suriname’s high level of public debt, the IMF provided a $468 million 2-year Standby-Arrangement (SBA). At that time, Suriname’s Ministry of Finance wrote that the IMF’s SBA would “provide a bridge to 2017 when new oil and mining production capacities are expected to be fully operational.” (*10)

After only $81 million of the IMF loan was disbursed, the IMF loan program was cancelled due to protests over the IMF’s austerity measures, which included increasing electricity prices. To replace the IMF loan, the government issued $550 million in bonds (including a significant bond issuance linked to the state-owned oil company, Staatsolie). The government appeared to be largely counting on future oil development in order to cover the bonds and other debt.

By 2020, the planned new offshore oil production still had not taken place. The COVID pandemic further exacerbated Suriname’s high, unsustainable public debt. In November 2020, Suriname defaulted on its public debt payments and turned to the IMF for financial assistance and budget support from the IDB and World Bank.

On December 22, 2021, the IMF approved a three-year $688 million Extended Fund Facility (EFF). Like in 2016, this funding provides a financial bridge until expected oil revenue will begin. If Total’s planned Final Investment Decision goes ahead by early 2022, the first oil production is expected to start in 2025. The IMF’s loan program will be disbursing funding from 2022 to 2024, i.e., during the planned oil development phase (see Graph 1).

On top of the IMF’s financial bridge, the IDB is proposing $300 million and considering a total of $500 million in budget finance to Suriname over the next three years during the oil development phase. In addition, the World Bank is considering $30 million to $100 million in budget finance over the next three years. Currently, the World Bank is proposing the first $30 million development policy operation (still without disclosing any program documents or prior reforms, even though the World Bank has been working with Suriname on this policy reform program since 2016). These are unprecedented amounts of budget finance to Suriname (see Graph 1). This budget finance will be given during the oil development phase and will not only provide a financial bridge, but could directly fund oil or gas development.

The IDB’s and World Bank’s proposed finance is given as non-earmarked budget support. Such budget finance can be spent on any oil- or gas-associated expenditure. The IDB and World Bank have a list of excluded expenditures for budget support, which includes items like weapons and nuclear-associated expenditures. However, oil, gas and coal are not on this exclusion list for either institutions’ budget finance. (Note: The World Bank’s pledge to no longer fund upstream oil and gas only applies to direct project finance, not budget finance, technical assistance or financial intermediaries.)

During the oil development phase, Suriname needs to raise funds for the oil development. The IFIs’ finance helps ensure the government’s finances are stable during the oil development phase when no oil revenue is coming in and oil development imports are high and exempt from duties/taxes. The government needs funding for management costs (e.g., assessing and issuing permits, auditing development costs, etc.), associated services and infrastructure. Stressed government finances, like the current debt crisis, can disrupt the oil development, which would add costs to the development and, thereby, reduce the profit. Hence, the importance of the IMF, IDB and World Bank’s huge public finance to Suriname during the oil development phase.

In addition, in August 2020, Reuters reported that Suriname’s state oil company, Staatsolie, had the right to acquire up to 20 percent of shares in Block 58. The stake would cost the company $1-$1.5 billion to purchase given total development costs of $6-$7 billion. (*11) The general manager of Staatsolie said it needed help from the state to raise the needed funds. (*12) The $1.3 billion injection from the IFIs would go a long way to support improving the credit rating needed to raise funds for the state’s participation in oil Block 58.

The IMF claims its loan program is not tied to new oil investments because the current debt restructuring terms are not based on future oil revenue. This is a misleading notion. The new IMF, IDB and World Bank loans will add substantial public debt, and repayment will not start until after the oil development phase. The debt sustainability of these unprecedented large loans is based on longer-term economic growth prospects of Suriname and the biggest planned development involves the new oil investments. Moreover, as already explained, the IMF program is also tied to the oil investments because it provides badly needed government funding during the oil development phase (see Table 2).

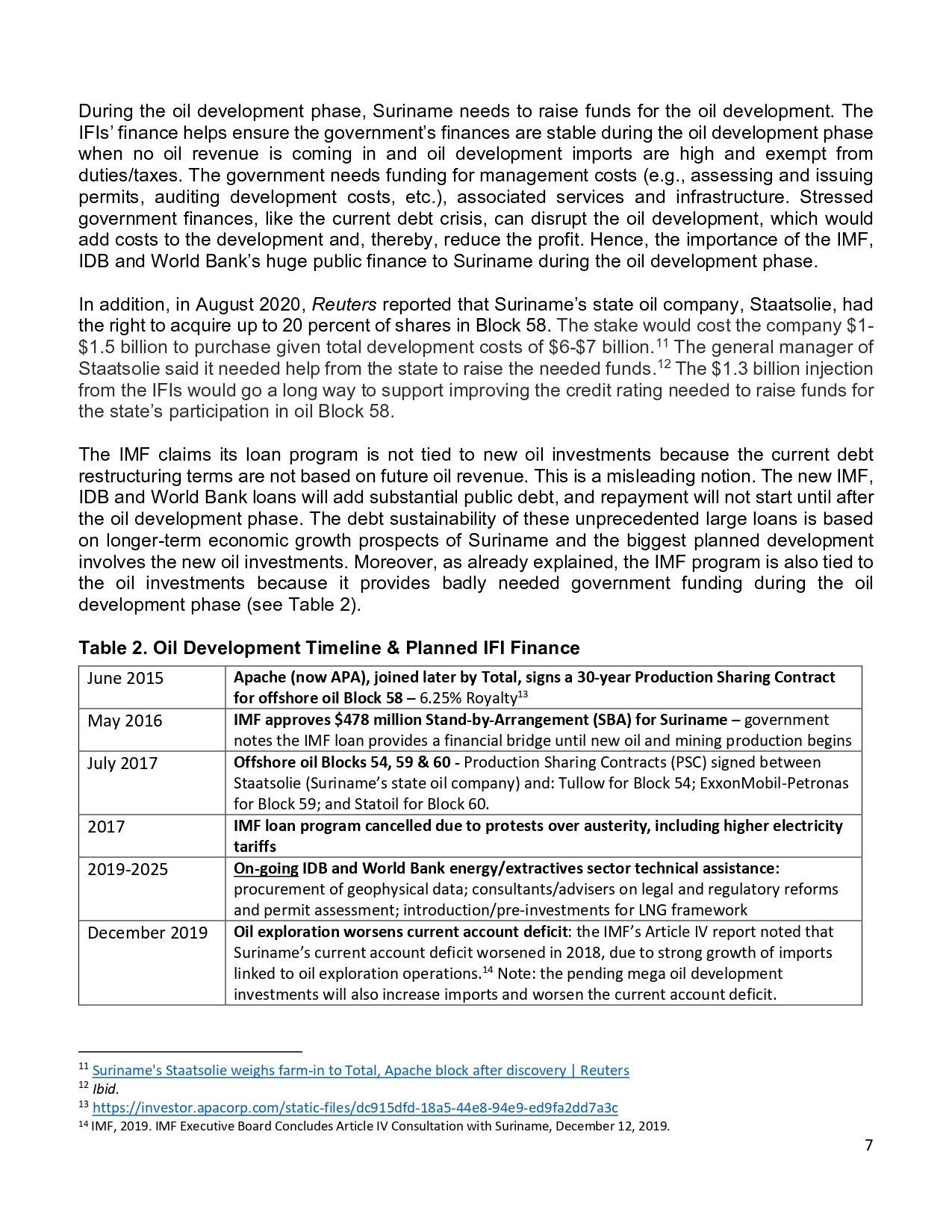

Table 2. Oil Development Timeline & Planned IFI Finance

| Date | Event / Description |

|---|---|

| June 2015 | Apache (now APA), joined later by Total, signs a 30-year Production Sharing Contract for offshore oil Block 58 – 6.25% Royalty (*13) |

| May 2016 | IMF approves a $478 million Stand-by Arrangement (SBA) for Suriname – the government notes the IMF loan provides a financial bridge until new oil and mining production begins |

| July 2017 | Offshore oil Blocks 54, 59 & 60 – Production Sharing Contracts (PSC) signed between Staatsolie (Suriname’s state oil company) and: Tullow for Block 54; ExxonMobil–Petronas for Block 59; and Statoil for Block 60 |

| 2017 | IMF loan program cancelled due to protests over austerity measures, including higher electricity tariffs |

| 2019–2025 | Ongoing IDB and World Bank energy/extractives sector technical assistance: procurement of geophysical data; consultants/advisers on legal and regulatory reforms and permit assessment; introduction/pre-investments for LNG framework |

| December 2019 | Oil exploration worsens current account deficit: IMF Article IV report notes that Suriname’s current account deficit worsened in 2018 due to strong import growth linked to oil exploration operations. (*14) The pending mega oil development investments are also expected to increase imports and further worsen the current account deficit. |

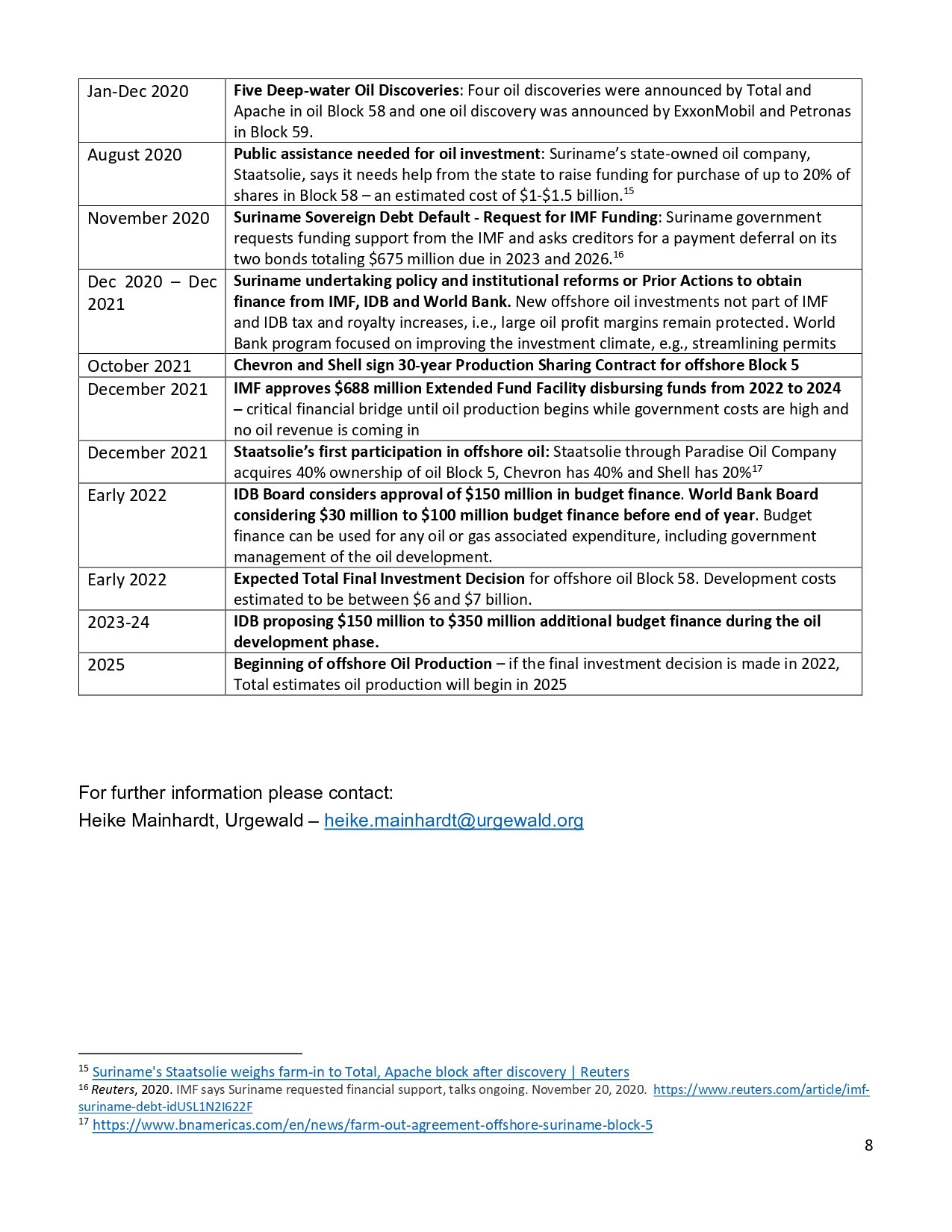

| Jan–Dec 2020 | Five Deep-water Oil Discoveries: Four oil discoveries announced by Total and Apache in oil Block 58, and one by ExxonMobil and Petronas in Block 59. |

| August 2020 | Public assistance needed for oil investment: Staatsolie says it needs state support to raise funds for purchasing up to 20% of shares in Block 58 – estimated cost $1–$1.5 billion. (*15) |

| November 2020 | Suriname Sovereign Debt Default – Request for IMF Funding: The government requests IMF financial support and asks creditors for a payment deferral on two bonds totaling $675 million due in 2023 and 2026. (*16) |

| Dec 2020 – Dec 2021 | Suriname undertakes policy and institutional reforms (“Prior Actions”) to obtain financing from the IMF, IDB, and World Bank. New offshore oil investments are not part of IMF/IDB tax and royalty increases, protecting large oil profit margins. The World Bank program focuses on improving the investment climate, e.g., streamlining permits. |

| October 2021 | Chevron and Shell sign a 30-year Production Sharing Contract for offshore Block 5. |

| December 2021 | IMF approves a $688 million Extended Fund Facility disbursing funds from 2022–2024 – a critical financial bridge until oil production begins while government costs remain high and no oil revenue is incoming. |

| December 2021 | Staatsolie’s first participation in offshore oil: Through Paradise Oil Company, Staatsolie acquires 40% ownership of oil Block 5 (Chevron 40%, Shell 20%). (*17) |

| Early 2022 | IDB Board considers approval of $150 million in budget finance; World Bank considers $30–$100 million before year-end. Budget finance may support oil/gas-related expenditures, including government management of oil development. |

| Early 2022 | Expected Total Final Investment Decision (FID) for offshore oil Block 58. Development costs estimated at $6–$7 billion. |

| 2023–2024 | IDB proposes $150–$350 million additional budget finance during the oil development phase. |

| 2025 | Beginning of Offshore Oil Production – if FID is made in 2022, Total estimates production will begin in 2025. |

Please check below a comparison of Projected vs. Actual Oil Development Timeline & IFI Finance!

For further information please contact: Heike Mainhardt, Urgewald –

- 1 https://www.idbinvest.org/en/projects/kuldipsingh-port-expansion-project-suriname

- 2 https://www.iadb.org/en/project/SU-L1065

- 3 https://www.nytimes.com/2021/01/20/business/energy-environment/suriname-oil-discovery.html

- 4 https://www.nytimes.com/2021/01/20/business/energy-environment/suriname-oil-discovery.html

- 5 Suriname has a population of less than 600,000 people.

- 6 https://www.sec.gov/Archives/edgar/data/1509991/000110465913080961/a13-19720_1ex10d20.htm; https://investor.apacorp.com/static-files/dc915dfd-18a5-44e8-94e9-ed9fa2dd7a3c; https://www.staatsolie.com/media/tuvjyme3/model-psc.pdf

- 7 https://www.nytimes.com/2021/01/20/business/energy-environment/suriname-oil-discovery.html

- 8 https://investor.apacorp.com/static-files/dc915dfd-18a5-44e8-94e9-ed9fa2dd7a3c

- 9 https://www.globaltaxjustice.org/en/latest/framing-feminist-taxation-making-taxes-work-women

- 10 Policy Letter to the IDB President from the Ministry of Finance of Suriname. April 28, 2016. Page 2. Policy Letter for the IDB / Policy-based Operation: Support to the Institutional and Operational Strengthening of the Energy Sector III https://idbdocs.iadb.org/wsdocs/getdocument.aspx?docnum= EZSHARE-1062625916-82

- 11 Suriname’s Staatsolie weighs farm-in to Total, Apache block after discovery | Reuters

- 12 Ibid.

- 13 https://investor.apacorp.com/static-files/dc915dfd-18a5-44e8-94e9-ed9fa2dd7a3c

- 14 IMF, 2019. IMF Executive Board Concludes Article IV Consultation with Suriname, December 12, 2019.

- 15 Suriname’s Staatsolie weighs farm-in to Total, Apache block after discovery | Reuters

- 16 Reuters, 2020. IMF says Suriname requested financial support, talks ongoing. November 20, 2020. https://www.reuters.com/article/imfsuriname-debt-idUSL1N2I622F

- 17 https://www.bnamericas.com/en/news/farm-out-agreement-offshore-suriname-block-5

Comparison of Projected vs. Actual Oil Development Timeline & IFI Finance

| Date | Projected Event / Description | Actual Developments | Divergence |

|---|---|---|---|

| June 2015 | Apache (now APA), joined later by Total, signs a 30-year Production Sharing Contract for offshore oil Block 58. | Contract signed; development plans initiated. | – |

| May 2016 | IMF approves a $478 million Stand-by Arrangement (SBA) for Suriname. | SBA approved; loan program later canceled due to social unrest. | Loan program canceled after disbursement of only $81 million; protests caused deviation from original plan |

| July 2017 | Offshore oil Blocks 54, 59 & 60 – PSCs signed between Staatsolie and partners. | Contracts signed; exploration activities commenced. | – |

| 2017 | IMF loan program canceled due to protests over austerity measures, including higher electricity tariffs. | Loan program canceled; alternative financing sought. | Confirmed deviation from projected IMF financing continuity |

| 2019–2025 | Ongoing IDB and World Bank energy/extractives sector technical assistance. | Technical assistance provided; projects initiated. | Minor delays in regulatory reforms due to pandemic disruptions |

| December 2019 | Oil exploration worsens current account deficit; IMF notes increased imports linked to oil exploration. | Current account deficit worsened; increased imports observed. | – |

| Jan–Dec 2020 | Five deep-water oil discoveries announced in Blocks 58 and 59. | Discoveries confirmed; exploration phase completed. | Slightly delayed reporting of discoveries to public |

| August 2020 | Public assistance needed for oil investment; Staatsolie seeks state support for purchasing shares in Block 58. | Staatsolie raises funds through bond issuance and loans. | Timing and scale of public financing differed from early projections |

| November 2020 | Suriname defaults on sovereign debt; requests IMF funding. | Default occurred; IMF Extended Fund Facility approved in December 2021. | IMF funding delayed by over a year; default occurred before funding secured |

| Dec 2020 – Dec 2021 | Suriname undertakes policy and institutional reforms to obtain financing from IMF, IDB, and World Bank. | Reforms implemented; financing secured. | Minor delays in disbursement; some reforms implemented later than planned |

| October 2021 | Chevron and Shell sign a 30-year PSC for offshore Block 5. | Contract signed; development plans initiated. | – |

| December 2021 | IMF approves a $688 million Extended Fund Facility disbursing funds from 2022–2024. | EFF approved; funds disbursed as planned. | Slightly delayed first tranche of disbursement |

| December 2021 | Staatsolie acquires 40% ownership of oil Block 5 through Paradise Oil Company. | Acquisition completed; participation secured. | – |

| Early 2022 | IDB Board considers approval of $150 million in budget finance; World Bank considers $30–$100 million. | Budget finance approved; funds allocated. | Approval and allocation occurred slightly later than projected early 2022 |

| Early 2022 | Expected Total Final Investment Decision (FID) for offshore oil Block 58. | FID announced on October 1, 2024; production start-up expected in 2028. | FID delayed by ~2 years; production timeline pushed to 2028 instead of 2025 |

| 2023–2024 | IDB proposes $150–$350 million additional budget finance during the oil development phase. | Additional financing approved; funds allocated. | Slight adjustments in amounts and timing of disbursement |

| 2025 | Beginning of Offshore Oil Production – if FID is made in 2022, production expected to begin in 2025. | Production expected to commence in 2028; development phase ongoing. | Production delayed by ~3 years due to FID delay and development scheduling |

Source:

Link:

Internal Link: